Do You Have Kids? You Need Term Life Insurance

If you have children who rely on your income, term life insurance is one of the simplest and most affordable ways to protect them. Here’s why parents need it, how much to consider, what it costs, and where term life fits into a smart family plan.

Key Takeaways

- If you have kids and people depend on your income, you likely need life insurance.

- For most families, term life offers the most coverage for the lowest cost.

- Employer-provided life insurance is often not enough by itself.

- Both working and stay-at-home parents usually need coverage.

- Buying younger and healthier typically means lower premiums.

- A 20- or 30-year term often lines up best with raising children and paying off a mortgage.

When I sit down with parents to talk about insurance, this is one of the clearest conversations I have: if you have kids and people depend on your income, you need life insurance. And for most families, the right place to start is term life insurance.

That may sound blunt, but I’d rather be direct than vague. Life insurance is not about you. It’s about the people who would be left behind if you died too soon. If your spouse would struggle to pay the mortgage, cover childcare, fund college, or simply keep the household afloat without your income, then life insurance is not optional. It’s part of responsible financial planning.

The good news is this: term life insurance is usually the most affordable way to buy a large amount of coverage when your family needs it most.

Why parents need life insurance

Once you have kids, your financial life changes. You’re no longer just covering your own bills. You’re supporting a family and protecting a future that may stretch 10, 20, or 30 years ahead.

If a parent dies unexpectedly, the surviving family may face:

- Loss of income

- Mortgage or rent payments

- Childcare costs

- Groceries and household bills

- Outstanding debts

- College savings gaps

- Funeral and final expenses

- The need for one parent to work less or stop working temporarily

That’s the practical side of life insurance. It creates a pool of money your family can use to keep going.

I’ve also seen families make a common mistake: they assume coverage through work is enough. In most cases, it isn’t.

Employer life insurance often provides 1 to 2 times your salary. For a parent with young children, that typically falls far short of what a family would actually need. It may also disappear if you change jobs.

What term life insurance is

Term life insurance is coverage that lasts for a set period of time, usually 10, 15, 20, or 30 years. If you die during that term, the policy pays a death benefit to your beneficiary.

If you outlive the term, the policy generally ends with no payout.

That’s the trade-off, and it’s exactly why term life is so affordable compared with permanent life insurance.

For parents, this makes a lot of sense. Your biggest financial obligations are often temporary:

- Raising children to adulthood

- Paying off a mortgage

- Replacing income during working years

- Covering college or major family expenses

A well-structured term policy is designed to protect your family during those high-risk, high-responsibility years.

Why term life is usually the right choice for families

In my experience, most young and middle-aged parents need the most coverage for the lowest cost. That is where term life shines.

Here’s a simple comparison:

| Feature | Term Life Insurance | Permanent Life Insurance |

|---|---|---|

| Coverage length | Set period, such as 20 or 30 years | Lifetime, as long as premiums are paid |

| Cost | Lower | Much higher |

| Cash value | No | Yes, usually |

| Best fit | Income protection for families | Long-term estate, legacy, or specialized planning |

| Coverage amount per dollar | Higher | Lower |

For most parents, the main goal is straightforward: if I die, can my family stay in the house and keep living their life?

If that’s the goal, term life is usually the best tool.

That doesn’t mean permanent life insurance is bad. It just means many families are better served by buying adequate term coverage first instead of underinsuring themselves with a small permanent policy because that’s all the budget allows.

How much term life insurance do parents need?

This is the question everybody asks, and the honest answer is: it depends on your income, debts, number of children, spouse’s earnings, and long-term goals.

A common rule of thumb is 10 to 15 times your annual income, but rules of thumb only go so far. I prefer to look at the real obligations your family would face.

Think through these categories:

1. Income replacement

How many years of income would your family need if you were gone?

For many families, this is the biggest factor.

2. Mortgage or housing costs

Would you want the home paid off, or do you simply want enough money to keep the payments manageable?

3. Childcare and daily living expenses

If a stay-at-home parent dies, the family may need paid childcare, transportation help, tutoring, or household support. That parent absolutely needs coverage too.

4. Debt payoff

Consider car loans, credit cards, student loans with cosigners, and personal loans.

5. Education funding

Some parents want the policy to help cover future college costs.

6. Final expenses

Funeral costs and related expenses can easily run $10,000 to $20,000 or more depending on arrangements.

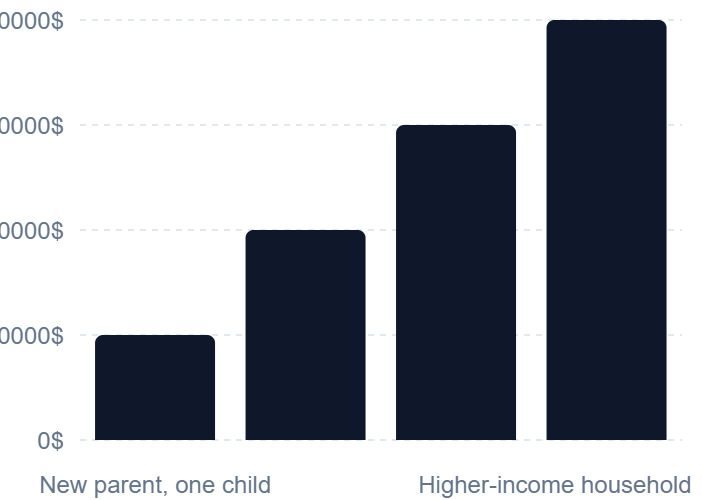

Illustrative coverage ranges for parents

These are not one-size-fits-all recommendations, but they’re reasonable starting points for many households:

| Household situation | Illustrative term coverage to consider |

|---|---|

| One child, moderate debt, one primary income | $500,000 to $1,000,000 |

| Two or more children, mortgage, growing income needs | $1,000,000 to $1,500,000 |

| Higher-income household or single-income family | $1,500,000 to $2,500,000+ |

| Stay-at-home parent needing childcare replacement value | $250,000 to $750,000+ |

The important part is not picking a number off the internet. It’s matching coverage to your real family situation.

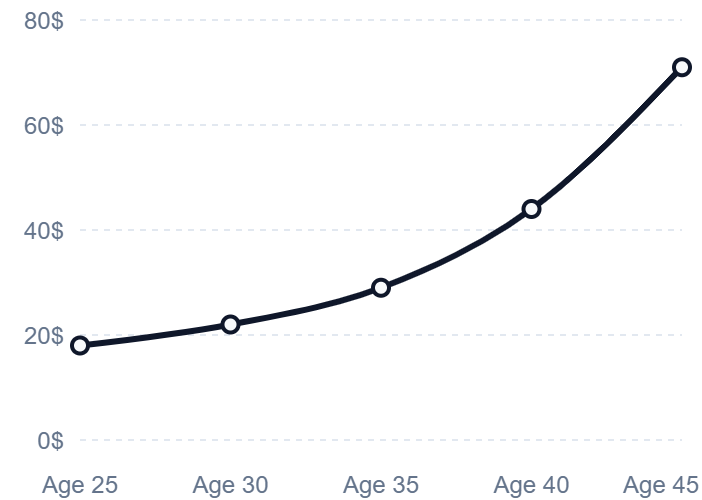

What term life insurance costs

Here’s what surprises a lot of parents: term life insurance is often much cheaper than they expected, especially if they buy while they’re healthy.

Age, health, tobacco use, coverage amount, and term length all affect cost. A healthy person in their 20s or 30s can often buy substantial coverage for a manageable monthly premium. Once health issues show up, rates can rise quickly.

That’s why waiting is risky. People tend to say, “We’ll do it next year.” Then next year turns into a diagnosis, a medication, or a higher rate class.

Illustrative monthly ranges for healthy non-smokers can look something like this:

- 30-year-old parent, 20-year term: often lower than many streaming and subscription bills combined

- 35-year-old parent, 20-year term: still generally affordable for many middle-income households

- 40-year-old parent, 20-year term: usually higher, but often still very cost-effective compared with the protection provided

I’m being intentionally careful here, because premiums vary by state, health, and underwriting. But the broad truth is simple: the younger and healthier you are, the more affordable term life tends to be.

Who needs coverage: just the breadwinner?

No. In many families, both parents need life insurance.

That includes:

- The higher earner

- The lower earner

- A stay-at-home parent

- A parent working part-time

I can’t say this strongly enough: a stay-at-home parent provides real economic value. If that parent dies, the surviving spouse may suddenly need to pay for:

- Full-time childcare

- After-school care

- Transportation help

- Meal support

- Housekeeping help

- Schedule flexibility or reduced work hours

That financial impact is very real, even if there was no paycheck attached.

How long should the term be?

For many parents, 20-year term or 30-year term makes the most sense.

A good rule is to choose a term that lasts through your biggest obligations, such as:

- Until your youngest child is financially independent

- Until the mortgage is mostly or fully paid off

- Until retirement savings are more secure

In general:

- 20-year term often fits parents with school-age children or a mortgage already underway

- 30-year term can make sense for younger parents with newborns or long financial runways

The biggest mistakes parents make

Over the years, I’ve seen a few patterns repeat themselves:

1. Waiting too long

The best time to buy life insurance is usually before you need it urgently. Health rarely gets better with age.

2. Relying only on work coverage

Employer coverage is helpful, but it is rarely enough on its own.

3. Insuring only one parent

Both parents often create economic value that needs protection.

4. Buying too little coverage

A small policy may feel better than nothing, but it may not truly solve the problem your family would face.

5. Focusing only on price

Cheap matters, but so do policy strength, conversion options, and the insurer’s underwriting process.

My honest advice to parents

If you have kids, don’t overcomplicate this.

Start with these questions:

- If I died this year, what financial problems would my family face immediately?

- How many years would they need support?

- Would my current coverage actually solve those problems?

- If not, what amount of term insurance would close the gap?

For most families, term life insurance is the clearest answer because it does exactly what parents need it to do: it buys a large amount of protection at a cost that usually fits the budget.

You hope your family never uses it. That’s the point. But if the worst happens, the right policy can mean the difference between financial stability and financial crisis.

And when you have children depending on you, that’s not a small decision. It’s one of the most important financial protections you can put in place.

Supporting Data

Frequently Asked Questions

How much term life insurance should I get if I have kids?

A common starting point is 10 to 15 times your annual income, but the better approach is to calculate your family’s actual needs. Look at income replacement, mortgage balance, childcare, debts, college goals, and final expenses. For many parents, that leads to coverage somewhere between $500,000 and $2,000,000 or more. The right number depends on your household income, your spouse’s earning ability, the ages of your children, and whether you want the policy to help pay off the house or fund education.

Is life insurance through my employer enough for my family?

Usually not. Employer life insurance often provides only 1 to 2 times your salary, which is rarely enough for a family with children, a mortgage, and long-term income needs. It can also be tied to your job, meaning you may lose or reduce that coverage if you leave your employer. Work coverage is a nice supplement, but most parents should not rely on it as their entire life insurance plan.

Do stay-at-home parents need term life insurance too?

Yes, in many cases they absolutely do. A stay-at-home parent may not bring in outside income, but they provide major economic value. If that parent dies, the surviving spouse may need to pay for childcare, transportation, housekeeping, meal support, and schedule flexibility that was previously handled at home. Term life insurance for a stay-at-home parent helps cover those replacement costs and gives the family breathing room during a very difficult time.

Should I buy 20-year term or 30-year term life insurance?

The right term length depends on how long your family will depend on your income. A 20-year term is often a good fit if your children are already in school and you’re further along on your mortgage. A 30-year term may make more sense if you have young children, a newborn, or a long financial runway ahead. In general, choose a term that carries your family through the years when they would be most vulnerable financially.

What is the downside of term life insurance?

The main downside is that term life does not last forever. If you outlive the term, the policy usually ends without a payout. It also does not build cash value the way permanent life insurance can. But for many families, that is an acceptable trade-off because term life is designed for one primary job: protecting dependents during the years when income replacement matters most. For that purpose, it is often the most efficient option.

When is the best time for parents to buy term life insurance?

As early as possible, ideally while you’re young and healthy. Life insurance premiums are based heavily on age and health, so waiting can cost you. Even a manageable health change, like high blood pressure, diabetes, or a history of smoking, can make coverage more expensive or harder to qualify for. If you already know your family would need financial help if you died, it usually makes sense to explore coverage sooner rather than later.

Jared Ullrich

Partner, Ullrich Insurance Agency

Jared Ullrich is the owner of Ullrich Insurance, along with his dad, Tom. Jared loves what he does and strives to make the most out of life every day. He has the best clients, the best team (team members at Ullrich Insurance), the best business partner, and he loves insurance. Jared has a wonderful wife and six kids. When he’s not helping Colorado families find the right insurance coverage, Jared is obsessed with doing cold plunges, spending time with the family, and going to the beach anytime he gets the chance.