Are E-Bikes Covered by Homeowners Insurance? An insurance guide for Colorado e-bike owners

By Jared Ullrich, Owner — Ullrich Insurance Agency

Important Insurance Disclaimer

This article provides general educational information only. Every homeowners insurance policy is different, and coverage varies by insurance company, policy wording, endorsements, and underwriting guidelines.

If you own any type of e-bike, you should contact your insurance agent and ask how your specific insurance company and policy treats e-bikes, including both property coverage and liability protection. Never assume coverage exists without confirming it directly with your insurer or agent.

Auto insurance will never cover an e-bike. If your e-bike is stolen, or if you injure someone while you’re riding your e-bike, your only chance for coverage is your homeowners insurance policy. There are a lot of restrictions.

Why This Topic Matters Right Now

E-bikes have become incredibly popular across Colorado. Families use them for recreation, commuters use them instead of cars, and many teenagers now rely on them for daily transportation.

But here’s something I’ve noticed as an insurance agent:

Many e-bike owners believe their homeowners insurance automatically covers them — and that is often not true.

Insurance companies don’t just look at whether something has pedals. They look at speed, motor capability, and risk, which is why e-bikes are divided into different classes.

And those classes matter a lot for insurance coverage.

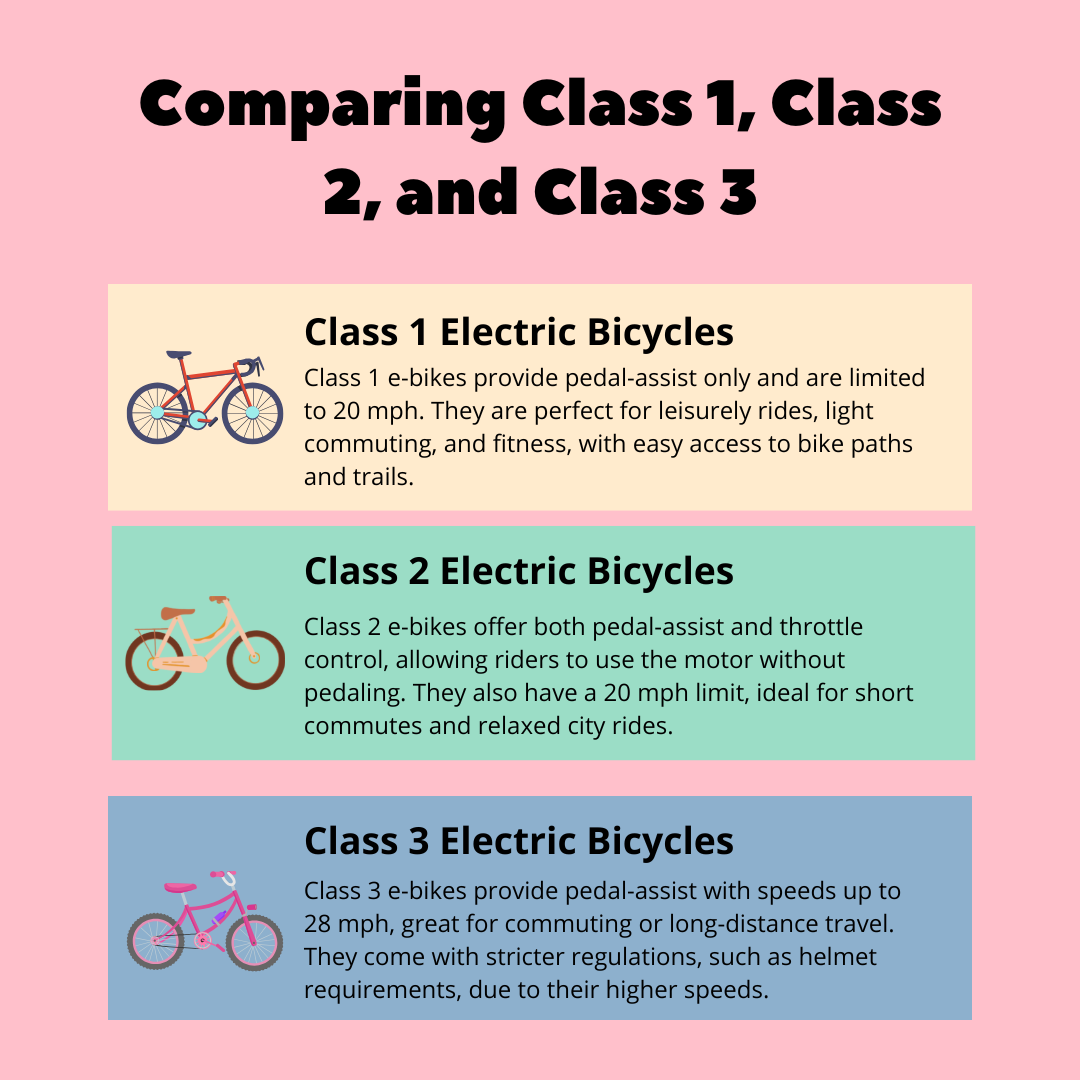

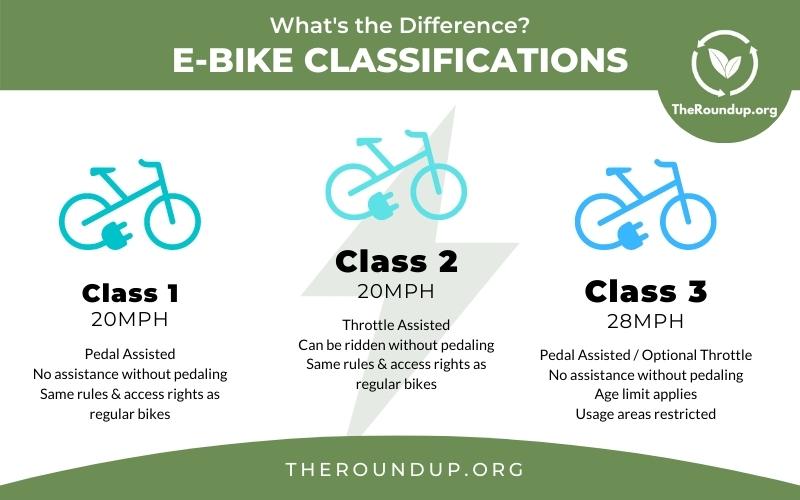

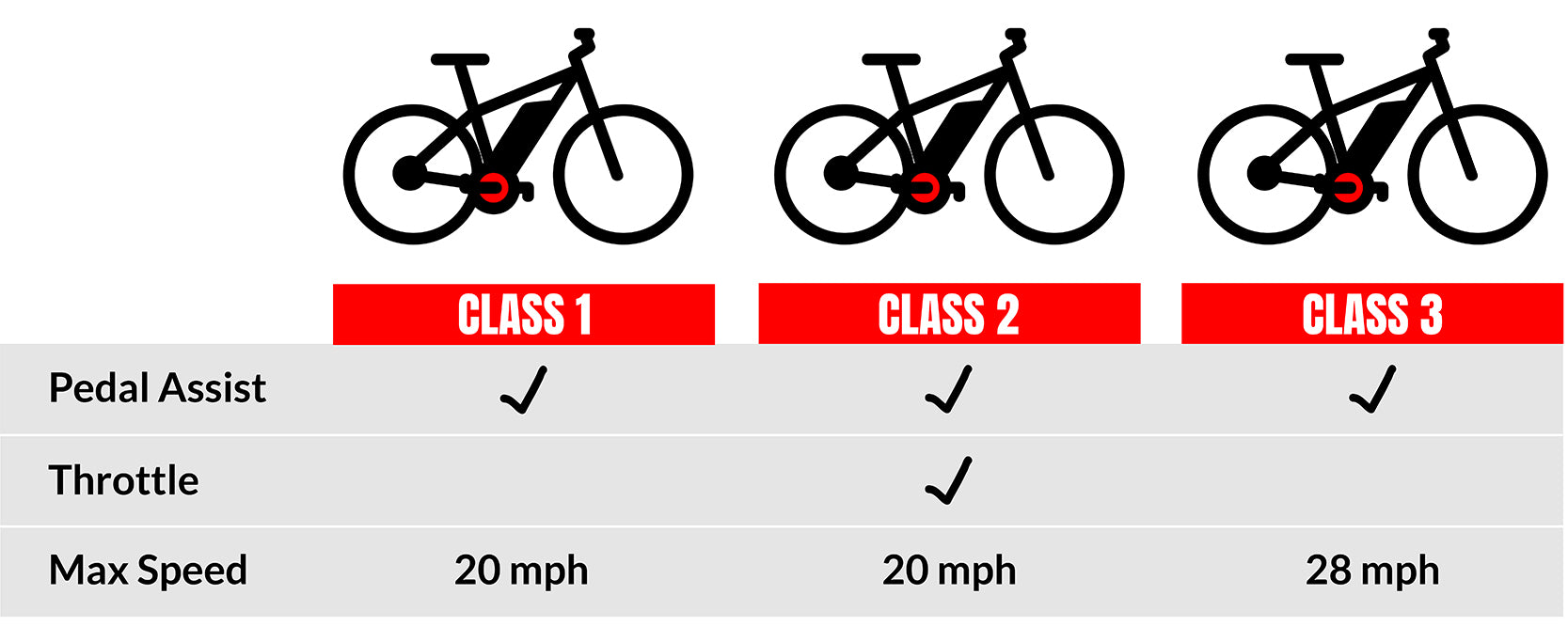

The Three Classes of E-Bikes (Insurance Overview)

Below is a simple visual explanation of how e-bikes are categorized.

4

Class 1 E-Bike

- Pedal assist only

- Motor works only while pedaling

- Assistance stops at 20 mph

- No throttle

Class 2 E-Bike

- Has a throttle

- Can move without pedaling

- Maximum assisted speed 20 mph

Class 3 E-Bike

- Pedal assist up to 28 mph

- Designed for faster commuting

- Often called a “speed pedelec”

How Insurance Companies View E-Bikes

Insurance policies were mostly written before modern e-bikes existed. Because of this, insurers ask one key question:

👉 Is this still a bicycle, or is it now a motorized vehicle?

As speed and motor power increase, insurance companies become less likely to treat the bike like ordinary personal property.

Class 1 E-Bikes — Usually Covered Under Homeowners Insurance

Class 1 e-bikes are typically the simplest from an insurance standpoint.

Because they require pedaling and stop assisting at 20 mph, most insurers treat them similarly to traditional bicycles.

What is usually covered

Homeowners insurance will often cover:

- Theft

- Fire damage

- Vandalism

- Covered accidental damage

Liability protection also usually applies if you accidentally injure someone while riding.

While coverage still depends on the individual policy, Class 1 bikes generally create the fewest insurance issues.

Class 2 E-Bikes — Coverage Can Be a Gray Area

Class 2 e-bikes introduce a throttle, meaning the bike can move without pedaling.

This is where policies start to differ.

Many homeowners policies exclude coverage for motorized land vehicles, and some insurance companies interpret throttle-powered e-bikes as falling into that category.

What I commonly see

- Property coverage may still apply

- Liability coverage may vary by insurer

- Policy wording becomes very important

If you own a Class 2 e-bike, it’s worth asking your agent specifically how your carrier classifies it rather than assuming coverage exists.

Class 3 E-Bikes — Typically NOT Covered by Homeowners Insurance

This is the biggest surprise for many owners.

Class 3 e-bikes can assist up to 28 mph, which significantly changes how insurance companies evaluate risk.

In most cases:

❌ The bike itself is not covered under homeowners insurance

❌ Liability coverage while riding is usually excluded

❌ Accidents involving the bike may fall outside your homeowners protection

From an underwriting perspective, these bikes begin to resemble motorized vehicles rather than bicycles.

If You Own a Class 3 E-Bike, You Typically Need Separate Insurance

If you want protection for a Class 3 e-bike, a separate policy is usually required.

Dedicated e-bike insurance policies may provide:

- Theft coverage

- Crash damage protection

- Liability coverage while riding

- Medical payments coverage

- Replacement cost options

Without separate coverage, many riders may unknowingly have little or no insurance protection while using the bike.

How to Find Out Which Class Your E-Bike Is

Many owners aren’t actually sure which class they own. Fortunately, it’s usually easy to determine.

Here are the best ways to check:

1. Look for the Manufacturer Label

Most e-bikes have a sticker or plate on the frame that lists:

- Class number

- Top assisted speed

- Motor wattage

This label is often near the crank, seat tube, or bottom bracket.

2. Check the Owner’s Manual or Manufacturer Website

Search your model name online along with:

“specifications” or “e-bike class”

Manufacturers almost always publish the classification.

3. Ask the Retailer Where You Purchased It

Bike shops typically know the class immediately.

4. Use These Quick Clues

- Pedal assist only → likely Class 1

- Throttle present → likely Class 2

- Assistance up to 28 mph → Class 3

This is something important that you need to figure out.

Common Coverage Mistakes I See

The most common assumption is:

“My homeowners insurance covers everything I own.”

That may be true for many household items — but e-bikes sit in a gray area between bicycles and motor vehicles.

Other surprises include:

- Expensive bikes exceeding property limits

- No liability coverage during accidents

- Teen riders increasing exposure

- Coverage limitations away from home

E-Bike Insurance Comparison by Class

| E-Bike Class | Homeowners Property Coverage | Liability Coverage |

|---|---|---|

| Class 1 | Usually covered | Usually covered |

| Class 2 | Depends on policy | Varies |

| Class 3 | Typically not covered | Usually excluded |

Questions Every E-Bike Owner Should Ask Their Insurance Agent

- Is my e-bike considered a motorized vehicle under my policy?

- Am I covered if I injure someone while riding?

- Is the bike covered for theft away from home?

- Do I need a separate policy?

Final Thoughts from Ullrich Insurance

E-bikes are a great innovation, but insurance policies haven’t fully caught up with how powerful some of them have become.

The simple rule I share with clients is:

👉 The faster the e-bike, the less likely homeowners insurance will cover it.

If you own a Class 3 e-bike, you should generally expect that separate insurance will be needed for both the bike and liability protection. However, if you own any e-bike at all, call our office and tell us the details and we will tell you how your homeowners insurance company will treat it.

A quick conversation with your insurance agent today can prevent a major surprise later.

—

Jared Ullrich

Owner, Ullrich Insurance Agency

Helping Colorado families understand coverage before claims happen.

Jared Ullrich

Jared Ullrich is the owner of Ullrich Insurance, along with his dad, Tom. Jared loves what he does and strives to make the most out of life every day. He has the best clients, the best team (team members at Ullrich Insurance), the best business partner, and he loves insurance. Jared has a wonderful wife and six kids. When he’s not helping Colorado families find the right insurance coverage, Jared is obsessed with doing cold plunges, spending time with the family, and going to the beach anytime he gets the chance.